Yesterday Apple announced two new phones (boring), a new smartwatch (mildly interesting) and old people playing rock music. They also introduced a payment system that could have a deep impact on the payment industry.

The system is called Apple Pay and it does some things a bit differently from existing mobile payment systems by leveraging Apple’s existing infrastructure. This includes a vast number of existing credit card numbers already registered with iTunes, TouchID – the fingerprint sensor and the Apple Watch.

Using Apple Pay

According to the information presented in Keynote and other stuff floating around the Internet, if you want to use Apple Pay for mobile payments, it works something like this:

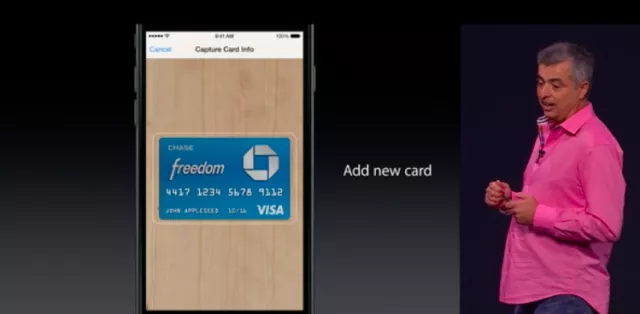

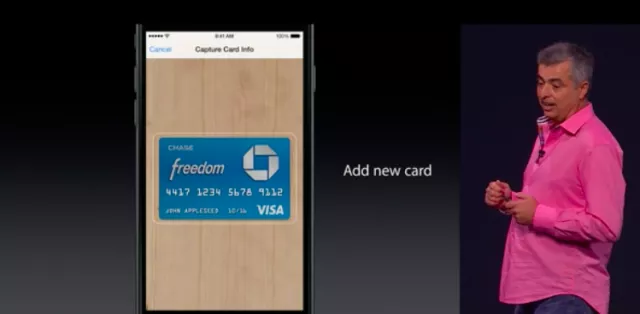

- You store your credit card number in the phone by taking a picture of the credit card. There’s an additional step here involved called “confirming your card”, but I’m not completely sure how it works (or why it’s needed at all).

- The phone stores this data in something called a Secure Element. I’m guessing it’s some sort of a crypto chip located in the phone. This means that, to get anything from the chip, you’ll need to place your finger on the Touch ID fingerprint sensor. This procedure basically makes everything more secure in case your phone gets stolen.

- If you have an iTunes account with a credit card linked (which almost everyone has), Apple Pay can use that credit card info. This is an enormous head start for Apple Pay, taking into consideration that there are around 800 million iTunes accounts.

Additional security layer

What’s not so obvious from the get-go is that Apple actually improved the security of credit card transactions with Apple Pay, as you don’t have to hand over your card to the cashier and use actual card numbers (you use something called Device Account Numbers).

To do this, they needed to achieve a new way of working with issuing banks, acquiring banks and credit card networks which is actually better than what we have now.

Will any credit card work?

Don’t think so. As it seems, only cards issued by Visa, MasterCards and American Express, and from a couple of selected US banks will work. Obviously, the list of banks/credit card networks should grow in time, but, for the time being, this just means that not every Visa, Master or American Express card will work. It probably has something to do with the additional security layer described earlier.

Pay in a store

The new phones (finally) have a NFC chip. You’ll be paying in stores by merely placing your phone next to a contactless terminal and then confirming the transaction with your finger on the Touch ID.

Contactless terminals aren’t a new thing. They’ve been around for some time now, but mostly in Europe (predominantly in the UK I would say).

What’s also cool here is that, if you have an Apple Watch, you can place it near the terminal and pay with the watch without taking out your phone.

Will this work in any store with a contactless terminal?

This is something I’m not very sure of. From the looks of it, the readers look like standard contactless POS terminals. On the other hand, they specifically list available stores on the website, so I’m not sure whether it’s possible to carry out payments in other stores that accept contactless payments, but are not in cahoots with Apple. I’m thinking – no.

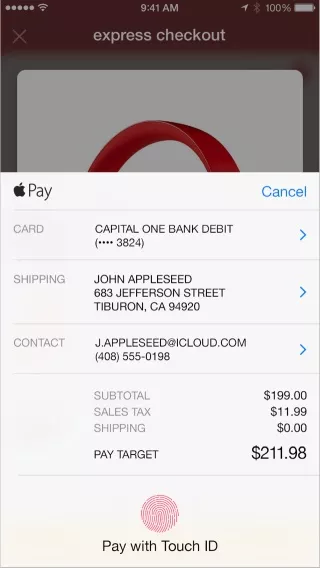

Pay in an app

This is where it gets interesting. Developers can use Apple Pay to integrate payment in their own apps. Where previously you had to develop special screens for users where they would enter their credit card details – now you hand that responsibility over to Apple Pay.

Also, when I first heard about this, my initial reaction was: ”Ok, but what about In-App Purchase?” Since Apple takes a 30% cut for every IAP, and (if we were to believe Tim Cook) they won’t take a cut with Apple Pay, we basically have two competing payment systems on the same platform and one of them leaves you 70% revenue.

Here’s the official info from Apple on this:

It is important to understand the difference between Apple Pay and In-App Purchase. Use Apple Pay to sell physical goods such as groceries, clothing and appliances. Also use Apple Pay forservices such as club memberships, hotel reservations and tickets for events. On the other hand, use In-App Purchase to sell virtual goods such as premium content for your app andsubscriptions for digital content.

It doesn’t say anywhere what happens if you try to sell Viber stickers via Apple Pay. Will your app be banned? Probably yes.

What ifs

Now, there are all kinds of potential “what ifs” here. What If I’m buying a book? I should obviously use IAP… But If I’m buying a digital book from the same merchant – Apple Pay? What if I’m buying a physical book with a digital copy?

What if I’m boosting a Facebook post? Virtual goods – yes/no/maybe? Apple will never make Facebook give them 30% of their revenue, but Facebook would surely use Apple Pay for this sort of thing, and leaving it out is not a great decision from a user experience standpoint.

It’s kinda messed up, and I don’t think Apple will want (in the long run) to have two very similar payment systems existing.

What payment processors can I use?

Apple gives you a couple of options. I like Stripe, but there are also others.

Other questions

- If I pay with an Apple Watch, how do I verify my fingerprint?

There’s no mention of the watch itself having a fingerprint reader (I’m fairly certain it doesn’t). Getting your phone out of the pocket to pay with your watch is stupid. But having a payment go through the watch without the fingerprint isn’t really the same level of security, so I’m not sure how this works.

- When can I start using it, what are the requirements for merchants?

This is obviously rolled out only to the US for now. Following how Apple typically works, I think it should be available in other parts of the world in a year or maybe more.

The terminals look like your typical contactless terminals. But again, the system works fairly differently from traditional credit cards so we’ll need to see what happens here.

Payment systems are a chicken and egg problem. You need merchants to get users using your payment system, but you also need users to get merchants motivated for investing in infrastructure.

Also, payment systems are heavily regulated, so issues with local regulation could creep out of the woodwork. I wouldn’t be surprised if 2-3 years would be a normal time frame for some countries, or even if Apple completely gave up on certain territories. Google Wallet still isn’t implemented everywhere.

What does all this mean?

But the main takeaway from all this is that the new improved checkout flow will certainly yield more conversions. I’m talking about drastic increase in sales here.

Basically – you’ll sell more stuff in your mobile app simply because people won’t need to enter their credit card details anymore.

What this also means is that more native e-commerce applications will be showing up. What was previously a web app will now probably become a native iOS app.

The reason is again simple – if your e-commerce application is a web application, your customer will need to re-enter their credit card details, but if it’s a native application with integrated Apple Pay – it will be a one-tap process.

Also, rest assured Apple will bring this to your Mac in the next iteration or the one after that. Just as soon as they iron out a secure user experience. So after that – you won’t have to punch in your credit card numbers while browsing on a desktop computer any more.

All of this could be potentially huge.

May you live in interesting times

Old Chinese Curse